It is not so clear that many mobile customers on new 5G networks are going to be receptive to faster speed tiers that are possible on such networks. It is not so clear that speed is a big problem on 4G networks in many markets, for example. But even where speed is perceived as an issue, standard 5G is a solution.

So much-faster 5G networks might satisfy demand using best effort mechanisms, especially since the 4G network might become a de facto standard service tier, with 5G becoming the premium service.

When the typical speed is perhaps 300 Mbps, it is not so clear how much demand might exist for faster-speed tiers that cost more.

On the other hand, in some markets, at some times, when congestion exists, the issue might not so much be “faster” speed, but “assured” speed minimums.

That will be a harder marketing proposition, but likely represents the new value possible on networks that can prioritize experience on a combination of “availability at all times.”

Already, many consumers say they find mobile data plans confusing. So adding another layer of complexity might not be welcome. For many, simpler usage plans might be more important than “speed.”

Perhaps 10 percent to 20 percent of U.S. mobile consumers would consider buying an internet access service that assures a minimum experience at times of congestion. Perhaps they will not, as standard 5TG will be an order of magnitude faster than 4G.

Be conservative and assume only about five percent to 10 percent would actually spend money for a service that guarantees bandwidth during times of congestion.

These assumptions are based on experience in other markets where we have some data on take rates for speed tiers. According to one study of rural fixed network internet access customers, 17 percent bought the fastest tier.

Some 20 percent of customers seem to have bought the fastest tier in New Zealand, while 15 percent bought the fastest tier in Australia. Still, it might be reasonable to expect that perhaps 10 percent of consumers will pay extra for the fastest speed tier.

One complicating issue is that most U.S. internet service providers offer faster speeds for the same price. That will show as consumer upgrading speeds, when in fact they remain on the same pricing tier.

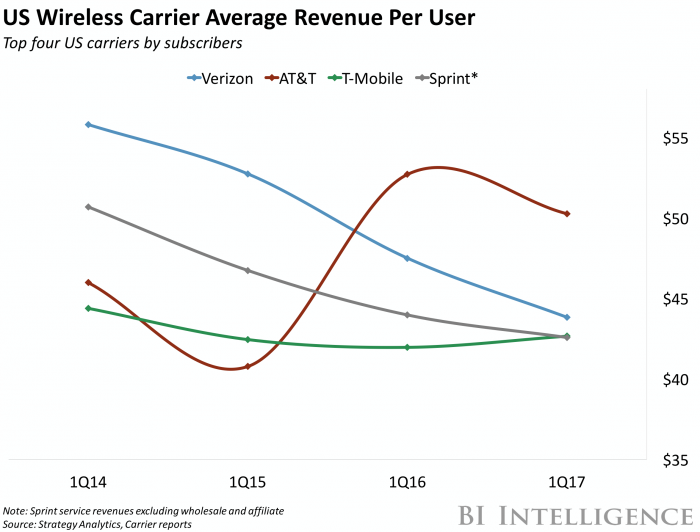

Assume an average monthly revenue per user of $45 to $50. So a 20-percent price premium would represent an incremental $9 per user to $10, per month, for perhaps five percent to 10 percent of customers.

Assume Verizon Wireless has 153.9 million accounts; AT&T Mobility 150.2 million; T-Mobile US 77.2 million and Sprint 53.5 million, for a total of about 435 million accounts.

Five percent of that is 22 million accounts; 10 percent is 44 million accounts. That suggests potential incremental revenue between $198 million per month to $$396 million per month in incremental revenue, or between $2.4 billion and $4.8 billion, a $9 per month revenue increase.

That is a meaningful amount of new revenue, if not a game changer. As always, additional benefits, such as reduced churn, longer customer relationship time or some possible impact on customer acquisition also would add to the upside.

No comments:

Post a Comment