Does the emerging market mobile business face a “new era?” And if it does, given that global telecom industry growth has been driven by emerging market mobile, does that portend a change in global telecom growth as well?

In brief, here is the thesis laid out by James Sullivan, J.P. Morgan head of Asia equity research (all of Asia except Japan): emerging market mobile now is revenue challenged, unable to generate new revenues at rates that justify current investments.

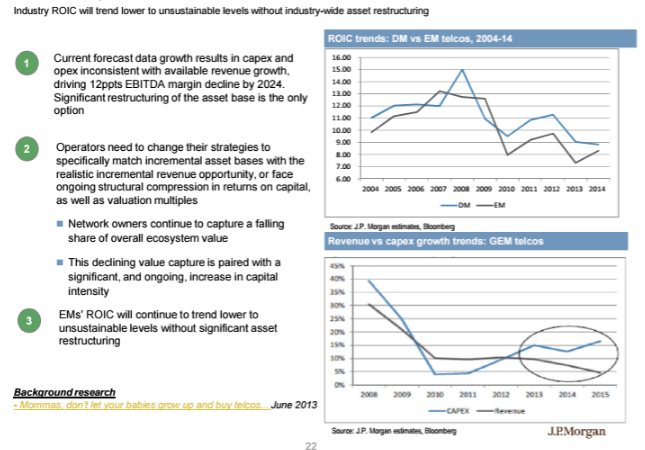

Since revenue cannot be increased, “asset restructuring” is necessary, to adjust the cost base. In emerging markets, that means surviving competitors will not be able to own their own facilities.

Emerging market mobile has faced several challenges, all based around limited revenue growth and higher capital investment that have grown faster than incremental revenue.

As mobile data revenues have grown, they have cannibalized voice revenues. Rapidly-increasing capital investment and operating expense have lead to declining earnings.

Source: J.P. Morgan

“Profitless growth” is perhaps one way to characterize the trend.

Sullivan will flesh out the thesis as one instructor among many appearing at the Industry Transformation Boot Camp, 18 September to 22 September, 2017 in Bangkok, including Spectrum Futures and PTC Academy components.

Sullivan sees signs that the restructuring has begun. You might look at India’s mobile market, where a huge consolidation of suppliers is underway.

The core thesis is that emerging markets have “no choice but to fundamentally change the structure of industry assets through the unification of networks via nationalization, centralization under a regulated return utility, or more aggressive commercial network sharing,” Sullivan argues.

For policymakers, there are a few fundamental options. In addition to nationalizing the networks, regulators could return to “regulated common carrier” models or oversee a reduction in capex by promoting network sharing.

That would presage a “new era,” indeed. Nationalization or a return to regulated rate of return would certainly lead to a reduction of physically-separate networks. Assuming no nation anymore can afford to run mobile networks on a permanent loss basis, and if revenue is too low, while costs are too high, then fewer assets is the solution.

That would create, in the mobile segment of the industry, the same pattern that exists for the fixed networks industry in many markets, where an authorized wholesaler supplies access capabilities to multiple retail providers.

In other markets, private actors might agree to share the cost of new investments, to reduce costs for each contender, as has been done for towers and radio infrastructure.

If Sullivan is right, the mobile market will be organized and regulated in very-different ways within a decade or so. For starters, the number of facilities will shrink drastically, which will have ripple effects across the whole ecosystem.

Still, “assets” are only part of the issue. Revenue models still must be addressed, and so far, nobody has sustainably proven how “access services” remains profitable, over time, when average revenue per account continues to drop.

Beyond that, there is the other key issue: whether top-line revenue growth can continue, and if so, what will propel that change.

No comments:

Post a Comment