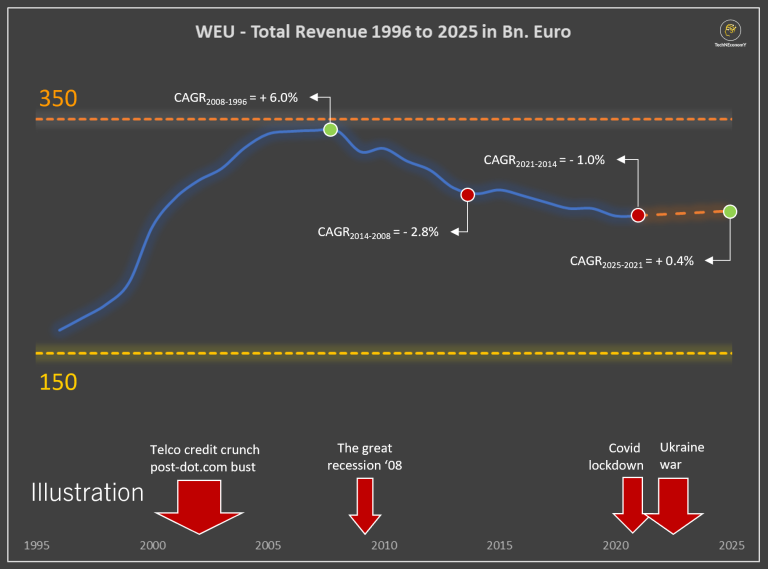

If you subscribe to the theory that every product has a life cycle, and if you are a mobile service provider, then this data on European mobile revenue should worry you. The reason is that the data fits the product life cycle suggesting that every product eventually reaches saturation and then declines.

And it that is true, the mobile business--in the most mature markets--faces product decline issues. One might well argue that the mobility business already has had to deal with such product life cycles. It replaced 1G (analog voice) with 2G, then 3G, then 4G and now 5G, with 6G coming in about eight more years, virtually indefinitely.

Subscriptions have been the mobile revenue driver, but the value proposition and revenue contributions have evolved over time. The value of a mobile subscription once rested solely on voice communications.

But average revenue per account began to decline in the 2G era, and growth came from text messaging. That revenue source, in turn, declined, to be replaced by mobile internet access during the 4G era. What changes in the 5G era is not yet decided.

One might also note other life cycles at work. Though subscriptions are essentially saturated in developed countries, subscription growth continues at a high level in other markets that have not yet reached saturation (virtually everyone has a mobile subscription).

The point is that European mobile operator revenue trends might suggest that “mobile device service” has reached a phase of decline, unless other new services can be created to run on the platform, as has happened in the past.

Perhaps metaverse or augmented or extended reality services could provide that driver. It is just too early to say.

We might also note product life cycles in the fixed networks business as well. Revenue once was driven by voice services, and profit by international and national long distance calling. As voice revenues dwindled some operators sparked growth by adding subscription TV, financial services or home security. Only linear video proved to be a major revenue driver.

With the decline of linear video, internet access has emerged as the growth driver. But even that product has reached saturation levels in many markets.

One might argue that internet access products also have changed, though. Dial-up internet access at kilobit-per-second levels arguably is a different product than access at megabit-per-second levels. Access at 100 Mbps arguably is a different product than gigabit-per-second access.

And multi-gigabit service arguably will be a different product than gigabit access. For fixed network operators, no less than mobility service providers, the issue is to keep finding new products with mass appeal, to replace maturing products.

Both mobile and fixed network services also have had business and consumer segments, though the business segment has been easier to delineate in the fixed, compared to mobile networks. In the fixed networks business, there are products that “only” businesses buy.

In the mobility access business, businesses have essentially purchased the same product, albeit with different packaging (volume discounts, more-detailed account tracking).

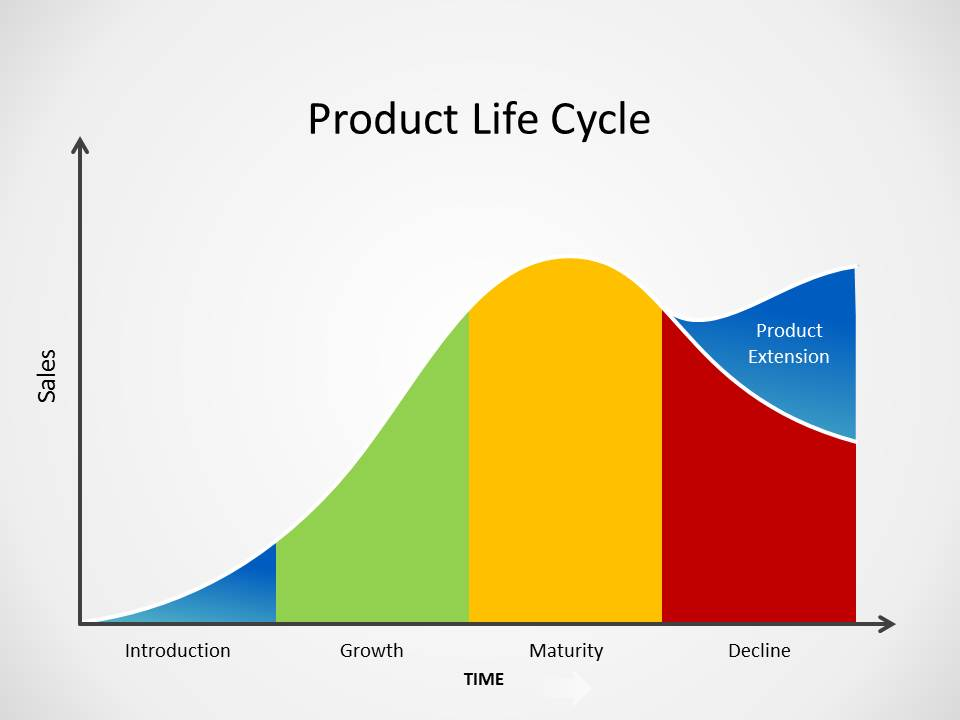

Here is a generic product life cycle illustration, with the possibility that product extensions can extend a product’s useful commercial life. Of course, some would argue that what is here noted as a “product extension” actually is a different product, with a different life cycle.

Think about mobile subscriptions. In that analogy, mobile voice is one cycle; text messaging another; mobile internet access a third. Others might argue that text messaging was a product extension, as was mobile internet access.

https://wholesalesuiteplugin.com/product-life-cycle/

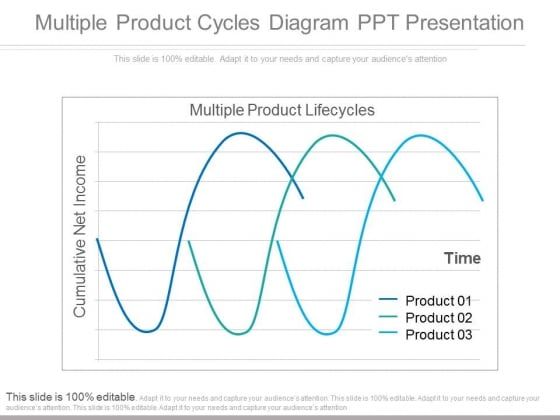

If one assumes text messaging and mobile internet access actually are different products from voice, albeit sold using the same common platform, then one has a sort of conceptual product roadmap. As product 01 reaches saturation--and before decline--work must have begun on product 02. Before product 02 reaches saturation, work must have begun on product 03, and so forth.

The big question we might ask is “what drives revenue growth after mobile broadband saturates?” If one views the mobile access network as a platform, what is the next big driver of revenue that can be developed on the platform?

Many would argue that internet of things, edge computing, private networks or network slicing are part of the answer. And they could help. On the other hand, it is hard to see any single one of those innovations driving total revenue the way that voice, messaging or internet access has done.

Applying the Pareto theorem, which generally is popularized as “20 percent of the instances drive 80 percent of the results,” ask yourself whether it seems possible that edge computing, private networks, IoT or network slicing could, at some point, drive 80 percent of total mobile operator revenue. If the answer is “no,” then those are not the drivers of the next wave of mobile operator revenue, in the mold of voice, messaging or internet access.

No comments:

Post a Comment