What is the financial state of the connectivity business, especially the mobility part of the business that drives most of the incremental revenue growth? Some might argue things are, if not fine, promising. Some mention 5G, the centrality of internet apps to support modern life and business, home broadband and other measures of connectivity importance as evidence the industry is well positioned to prosper.

Service providers themselves, in asking for payments for a few hyperscale app and content providers, basically argue matters are not fine, and that internet service providers require taxes on some interconnected internet domains to remain solvent.

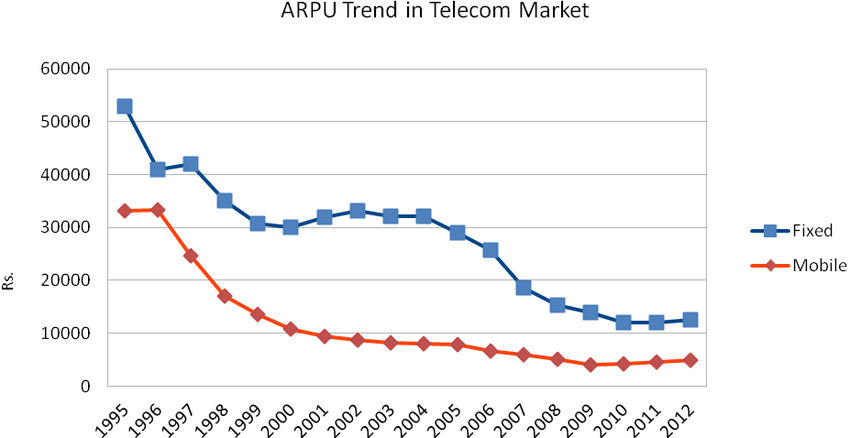

By most financial measures, the business has gotten tougher for several decades, though “telecom” never was a fast growth industry, so slow revenue growth is not unusual, on the order of two percent a year, though some estimates peg growth at higher rates, especially in Asia-Pacific region, for example. Revenue and profit margins remain issues, though.

Profits, though, are another matter. The average service provider profit margin around 12.5 percent is typical, and not unusual for many industries.

Since the global industry moved from monopoly to competition, excess profits have been removed, though by some measures, including growth in lesser-developed regions and including new contestants and well as legacy service providers, profit levels might be higher, globally, than in 1995, for example.

Also, the global averages can conceal higher or lower growth rates in various regions, as well as differing performance by company.

All that, however, does affect public market valuation and capitalization, as market multiples are assigned by expectations about revenue growth. The lower the multiple, the lower the valuation and market cap. And since equity value is currency, a firm with low-value currency will have a tough time buying a firm with high-value currency.

That explains why most telcos cannot afford to acquire assets of the likes of Facebook, Google, Apple or Amazon.

More significant, though, is the rise of the internet, which operates on a disaggregated basis, using layers that are conceptually distinct and business functions that are handled by different parts of the value chain and ecosystem.

In other words, users can access applications and services that are not “owned” by a connectivity provider, as once was the case. App providers do not need either permission or a formal business relationship with any internet service provider to connect with users and customers.

That is the main meaning of the term “over the top.” App providers can go straight to their users and customers over any lawful local internet connection. That also affects connectivity provider options, as it no longer is possible to create walled garden apps that are tied to a particular ISP.

And though connectivity providers likely would prefer to be in the applications and commerce parts of the ecosystem, given the higher growth and profit margins, repositioning in that way is difficult. Ignoring for the moment domain knowledge and skills, gaining a substantial position in the applications part of the internet ecosystem is financially daunting.

Because the at-scale hyperscalers have market valuations that are higher than that of connectivity providers, and because those revenues carry higher market multiples, the cost of acquiring a major position is unrealistic.

In recent years we have watched AT&T, for example, spend heavily--and borrow heavily--to support movement into local access, content and linear video. Ultimately, those efforts failed as the debt burdens could not be carried.

Some earlier acquisitions--of mobility assets, for example--have worked out much better, in large part because organic growth was possible. Scale could be built, rather than having to be acquired.

The bottom line is that the current state of the global connectivity business is not completely clear. Growth is higher in developing regions; quite low in developed regions. Again, that is not historically unusual at all. What we used to call “telecommunications” always was a slow-growth industry.

In the competitive era, growth is more important as legacy market share is lost to new competitors. It is akin to a leaky water bucket. New water has to be poured in at the top since water continually leaks out the bottom of the bucket.

No comments:

Post a Comment