Whether 5G will enable new revenue streams for mobile service providers has been a big concern, in a few different senses. The first question is ”will operators earn a payback on investments in 5G?” The second question is “if so, how will operators earn a payback?”

A third question might be “are there new sources of revenue, as well?”

The questions get asked for many of the same reasons telcos used to get asked about investments in fiber to the home. Given that a huge capital investment has to be made, with money borrowed to support the investment, will the investment pay off?

The mobile industry and fixed networks segments of the connectivity industry provide different answers. For fixed network service providers, the answer really does turn on what new revenue sources can be provided, compared to the cost of the investment. Video entertainment and high-speed internet access are the traditional answers.

Mobile operators have different answers, essentially. Capex in the next generation network actually is required simply to maintain the base business.

In the internet era, access bandwidth is critical and ever growing in terms of customer consumption. Without the ability to supply additional bandwidth at lower costs per bit, the core business itself is challenged.

In one sense, that means there is a simple answer for the question of whether the capex has a payback. Over time, every customer migrates to the next generation network and the older networks are decommissioned. So the payback for 5G comes from former 4G subscriptions, which in turn were driven by conversions of 3G subscriptions, which earlier were generated from 2G upgrades.

That also answers the second question. To stay in business, mobile operators have to upgrade their networks to supply their existing customer requirements, and have done so every decade since the advent of 2G.

New incremental revenue streams have arisen in each generation, though not always anticipated. Text messaging arrived with 2G. Internet access arrived with 3G. Mobile web and video arrived with 4G. So the issue is “what about 5G?”

At this point, the betting is that most of the new incremental revenue will come from enterprise use cases: internet of things; edge computing and customized private networks enabled by network slicing.

Some also envision a change of business model. Today’s revenue model is as Strategy & illustrates below. Mobile operators sell connectivity services to customers, who use that connectivity to buy and use apps supplied by third parties. 5G, as such, does not change the model.

At least potentially, that could change. Some argue that mobile operators could sell some types of services directly to enterprises for incorporation into their own products. Edge computing or internet of things provide the best examples of that.

In contrast to today’s model, where customers (consumer or business) buy internet access for their own use, network slicing might be purchased by enterprises to support the creation of new services that are sold directly to customers (business or consumer).

Examples would be video entertainment services, where revenue is earned by providing content, and the use of the network is a feature; IoT services, where the fee is earned for providing monitoring, analysis and adjustment, not “connectivity;” or edge computing, where the cost of device connections is embedded in the cost of the edge computing.

At least in principle, the process could work the other way, where a telco incorporates third-party features into a complete solution, then sold to customers under the telco’s brand name.

None of the solution provider business models require any fundamental change of how mobile operators operate. They continue to sell “access” to enterprises, though possibly for enterprise resale.

Or the reverse could happen, where mobile operators source third party capabilities to create branded solutions and services. In principle, that still could be described as the “typical business model” illustrated in exhibit 4.

There is one other scenario not shown. A mobile operator might, in some cases, be able to create an indigenous, “home grown” capability, rather than sourcing externally. Though perhaps rare, it is conceivable.

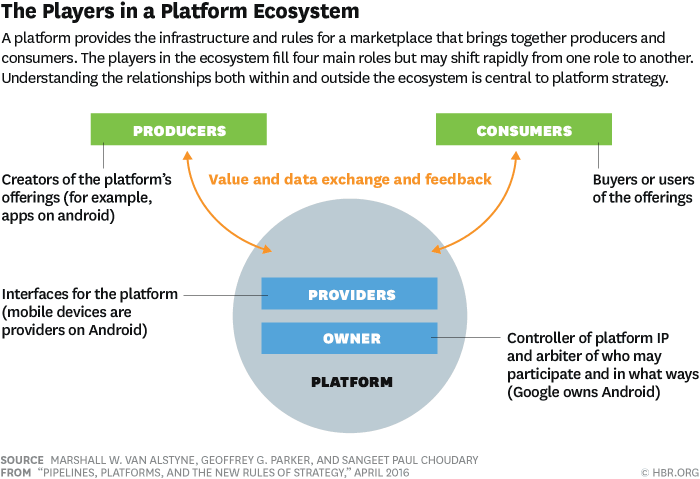

The truly radical departure would have the former connectivity provider converting (somehow) to a platform business model. In that asset light scenario, the revenue model is transactions, not connectivity as such.

source: Platform Business Model

That really is different. As shown below, the traditional “sell capacity” model is direct and asset heavy. In this model, a firm creates and sells services under its own brand name. In a full platform business model, revenue is created primarily by transactions on the platform.

It is asset light in the sense that what is bought and sold is not “owned” by the platform. Transaction volume--not customer accounts per se--becomes the key revenue metric.

source: Platform Business Model

So back to the questions, 5G almost certainly will create new revenue sources, in addition to replacing existing products sold to existing customers. At the moment, most agree that will happen as enterprises create new products based on use of IoT and edge computing.

Mobile operators will benefit directly by selling additional products to enterprises creating those services. In other cases, mobile operators will themselves create branded solutions and services in the IoT and edge computing areas.

The wild cards are unexpected use cases that almost certainly will emerge, as was the case for prior mobile generations since 2G.

No comments:

Post a Comment