Some business patterns are remarkably far ranging. Consider the product life cycle, the S curve or their impact on connectivity product and revenue sources over time.

The S curve has proven to be among the most-significant analytical concepts I have encountered over the years. It describes product life cycles, suggests how business strategy changes depending on where on any single S curve a product happens to be, and has implications for innovation and start-up strategy as well.

Some say S curves explain overall market development, customer adoption, product usage by individual customers, sales productivity, developer productivity and sometimes investor interest. It often is used to describe adoption rates of new services and technologies, including the notion of non-linear change rates and inflection points in the adoption of consumer products and technologies.

In mathematics, the S curve is a sigmoid function. It is the basis for the Gompertz function which can be used to predict new technology adoption and is related to the Bass Model.

I’ve seen Gompertz used to describe the adoption of internet access, fiber to the home or mobile phone usage. It is often used in economic modeling and management consulting as well.

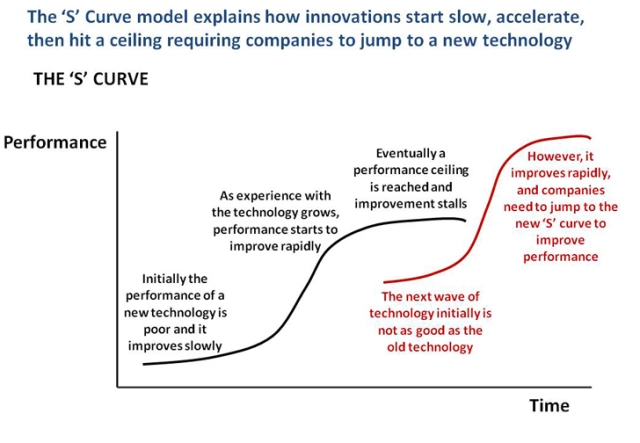

The following graph illustrates the normal S curve curve of consumer or business adoption of virtually any successful product, as well as the need to create the next generation of product before the legacy product reaches its peak and then begins its decline.

The graph shows the maturation of older mobile generations (2G, 3G) in red, with adoption of 4G in blue. What one sees is the maturing products are the top of the S curve (maturation and decline) while 4G represents the lower part of the S curve, when a product is gaining traction.

The curves show that 4G is created and then is commercialized before 3G reaches its peak, and then declines, as the new product displaces demand for the old.

Another key principle is that successive S curves are the pattern. A firm or an industry has to begin work on the next generation of products while existing products are still near peak levels.

It also can take decades before a successful innovation actually reaches commercialization. The next big thing will have first been talked about roughly 30 years ago, says technologist Greg Satell. IBM coined the term machine learning in 1959, for example.

The S curve describes the way new technologies are adopted. It is related to the product life cycle. Many times, reaping the full benefits of a major new technology can take 20 to 30 years. Alexander Fleming discovered penicillin in 1928, it didn’t arrive on the market until 1945, nearly 20 years later.

Electricity did not have a measurable impact on the economy until the early 1920s, 40 years after Edison’s plant, it can be argued.

It wasn’t until the late 1990’s, or about 30 years after 1968, that computers had a measurable effect on the US economy, many would note.

The point is that the next big thing will turn out to be an idea first broached decades ago, even if it has not been possible to commercialize that idea.

The even-bigger idea is that all firms and industries must work to create the next generation of products before the existing products reach saturation. That is why work already has begun on 6G, even as 5G is just being commercialized. Generally, the next-generation mobile network is introduced every decade.

What is true of connectivity provider revenue also is true of firms. My general rule of thumb is that service providers must replace half of all present revenue every 10 years. As it turns out, about half of all Standard & Poors 500 companies are replaced every decade.

The typical S&P 500 firm remains on the index less than 20 years, and is predicted to drop to about 14 years by 2026, says Innosight.

Shrinking lifespans are in part driven by a complex combination of technology shifts and economic shocks. “But frequently, companies miss opportunities to adapt or take advantage of change,” Innosight says.

“For example, they continue to apply existing business models to new markets, fail to respond to disruptive competitors in low-profit segments, or fail to adequately envision and invest in new growth areas, which in some cases can take a decade to pay off,” Innosight notes.

The point is that “no business survives over the long-term without reinventing itself,” Innosight says. That seems also true of connectivity firms.

The next era of telecommunications might be a stretch for most firms, in the sense that revenue growth might have to come from application creation and development that never have been core competencies.

But some seem to have unrealistically high hopes for 5G.

To be sure, edge computing, internet of things use cases and a few consumer use cases involving artificial reality or virtual reality seem promising. The larger point is that revenues in any of those new growth areas will not likely be enough to offset stagnating revenues in the core connectivity business. They will help, but the magnitude of new revenue growth will be staggering.

If we assume that past patterns hold, and that most telcos will have to replace half of current revenue each decade, then any new revenue sources have to be big. And that is the issue.

Edge computing, internet of things or private networks will help. But are they big enough new revenue sources to replace literally half of current revenue? Some might argue that is unlikely.

Incremental gains are not going to be enough. Telcos are looking at generating new revenues to the tune of $400 billion in the next 10 years. If IoT or edge computing generate $10 billion to $20 billion in incremental new revenues, that helps. But it does not come close to solving the bigger revenue problem.

Whether at the firm level or the product level, change is a constant. Half of what revenue drives a connectivity business in a decade does not yet exist, or is not yet tangible. Up to half of the product drivers of that revenue do not exist or have not yet been mass deployed.

No comments:

Post a Comment