The "rule of three" might be used as a tool to separate stable telecom services markets from those which arguably are more unstable and could see change.

The reason is that, in a stable market, the second-biggest potential challenger cannot hope for an active attack on the leader to succeed. The market share and profit difference between number one and number two is simply so great that the challenger risks bankruptcy if it launches a major price assault, for example.

The number-one provider would simply match the price reductions and, though taking a profit hit, is better positioned to survive than the challenger, which might very well see all profit vanish. Roughly the same calculation can be made by the number-three provider, which is so much smaller than number one and number two that it likewise would have a nearly-impossible challenge were it to launch a serious attack.

That creates a major barrier to the number-two or number-three provider launching a vigorous price-related or value-related assault. The reluctance to upset the market also helps account for market stability.

Stable industries tend to have a distinct market share pattern, as noted by Bruce Henderson, founder of the Boston Consulting Group. "A stable competitive market never has more than three significant competitors, the largest of which has no more than four times the market share of the smallest,” Henderson argued.

Sometimes known as “the rule of three,” he argued that stable and competitive industries will have no more than three significant competitors, with market share ratios around 4:2:1.

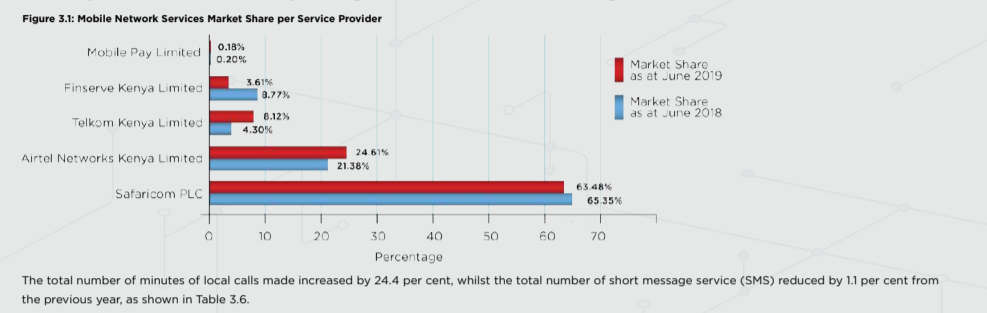

The mobile services market in Kenya illustrates that pattern, where Safaricom, the market leader, has more than twice the share of the number-two provider Airtel, which in turn has twice the share of the number-three provider Telekom Kenya. That same pattern tends to hold for profit margins as well.

source: Communications Authority of Kenya

One sees this pattern in some telecom markets. Looking at market share and return on invested capital for the three largest telecom providers in Thailand, China, and Indonesia since 2015, you can see that financial return and market share tend to be directly related.

The real-world structure does not precisely match the rule of three predictions, of course, with Thailand having the almost-perfect correspondence between predicted results and actual results, according to a 2016 analysis by Reperio Capital.

In many other markets, two observations are apt: where the 4:2:1 pattern does not exist, markets either are not competitive, or not stable, or both. And though we might be tempted to think such patterns exist mostly for capital-intensive industries, the pattern seems to hold in most industries.

Source: Reperio Capital

My rule of thumb incorporating the “rule of three” is that the leader has twice the share of number two, which in turn has twice the share of provider number three. In Thailand, the general pattern holds.China and Indonesia do not fit the stable pattern so well.

In Thailand the pattern holds well. The leader has 53 percent share, number two has 31 percent and number three has 17 percent share.

If those markets are actually competitive, some further change in market share would be expected, with the market leader losing share, gained by a clear and stronger number two.

No comments:

Post a Comment