Given the huge differences in proposed use of 5G spectrum (low band, mid band, high band), it probably is not surprising that mobile operator architectural choices are disparate. It makes a huge difference whether new 5G efforts are anchored by low band or high band spectrum, for example.

Nor, given pressures in the business model, should we be terribly surprised that 5G investments are being carefully phased to match existing business models, while investment in the more-futuristic use cases is delayed.

Basically, that means most 5G investments, by most mobile operators, will be for capacity overlays to sustain the current consumer mobile broadband business. In a smaller number of cases, where a new use case is deemed feasible (fixed wireless out of region), 5G investment will aim to support a brand-new revenue stream. But the emphasis is on tapping existing demand, not supporting exotic new use cases of uncertain scale.

The best example is Verizon’s fixed wireless assault, and a possible similar attack by T-Mobile US, should its merger with Sprint be approved. Verizon sees an addressable market of perhaps 30 million homes. At a 20-percent capture rate, that implies a customer base of six million.

Assume a blended average revenue per account of $60 a month. That implies annual account revenue of $720. At six million accounts, Verizon would generate $4.3 billion in incremental revenues from access services.

T-Mobile US has argued it could gain 9.5 million new fixed wireless accounts. At the same $60 a month rate per account, that suggests an incremental $6.8 billion in annual revenue.

A new market representing revenues of $11 billion in the saturated consumer market is no small thing. Just as important, that revenue does not require discovery of some new consumer need; only a shifting of market share.

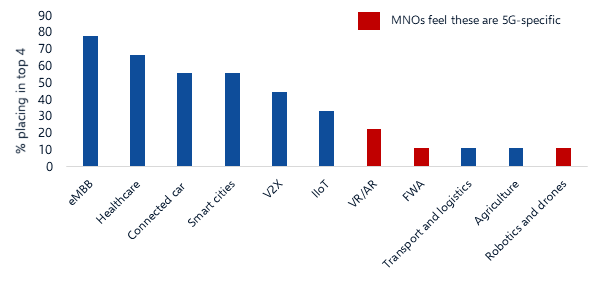

With that exception, “early 5G will be all about consumer mobile broadband delivering high speed to the handset, and ignoring new business models,” says Caroline Gabriel, Rethink Technology Research analyst.

In a new survey, Rethink Technology Research found that “the top goal for first phase 5G deployment are cost related, namely to support lower cost mobile broadband services, and mostly to support the enhancement of conventional use cases.

That should not come as a big surprise. Most tier-one service providers are public companies, with a necessary obligation to show that investments generate a reasonable return in a reasonable amount of time. That always creates pressure to show rather-immediate returns.

And so long as capital investment can be phased, and basically held within the constraints of typical annual capex levels, there is far less business risk.

Service provider executives are a practical lot, taking prudent risks they can justify to financial markets. So, with the exception of 5G fixed wireless, which is a new use case, most of the initial 5G investments will target mobile broadband services.

To some extent the upside comes from required capacity improvements that must be made in any case. To some extent the upside will come from higher mobile broadband revenues, created by higher-priced services whose value is greater mobile internet access usage buckets or faster speeds or both.

No comments:

Post a Comment