AT&T's acquisition of Time Warner is going to remain controversial for some time, as was AT&T's purchase of DirecTV. But that latter move (even if still controversial in some quarters) arguably achieved its goals.

With the passage of enough time, we now can assess the “fear” or “hope” around the AT&T acquisition of DirecTV.

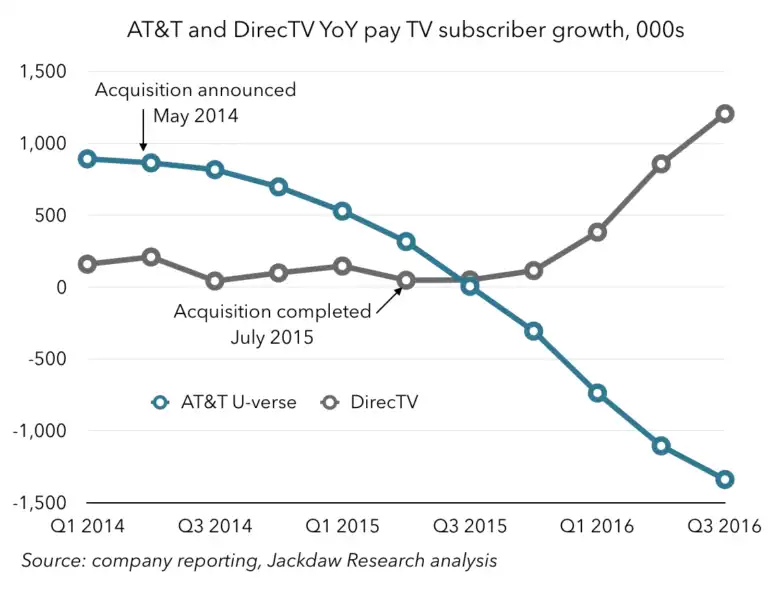

The fear in some quarters was that AT&T was about to substitute DirecTV as its video subscription driver, deemphasizing U-verse. About a year after the acquisition closed, the results were clear enough: DirecTV was growing and U-verse was shrinking.

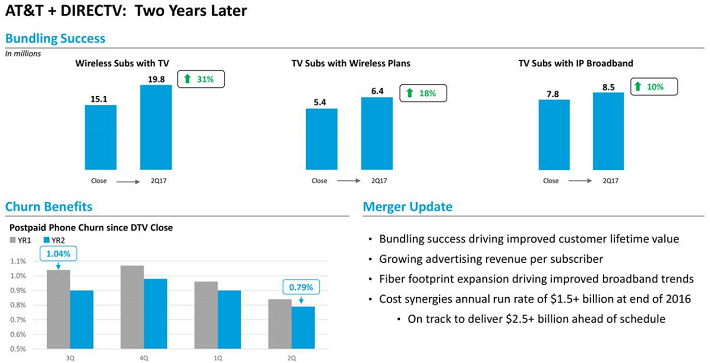

The acquisition, in turn, allowed AT&T to increase revenues (and reduce churn) from bundling, across its fixed, mobile and satellite platforms. Perhaps the biggest change was that the new entertainment video service helped boost revenue in the mobile segment of the business.

Mobile customers buying video grew significantly, as did entertainment video customers who chose AT&T for mobility services.

Some still worry that entertainment video is a trap, as linear subscriptions fall out of favor and streaming products replace them. DirecTV Now's success is part of the rationale for believing that the linear platform, throwing off cash flow now, also is a strategic underpinning for the next waves of growth from content and advertising.

The Time Warner acquisition throws that earlier DirecTV acquisition into sharper relief.

Some of the changes in DirecTV versus U-verse video might be attributable to the decline of the linear video business overall. Some of the change is because of different AT&T marketing priorities. But much of the difference is from scale. AT&T’s U-verse network only reached a fraction of AT&T’s total fixed network base.

DirecTV meant that AT&T can sell nationwide, in region or outside it.

Even before the launch of DirecTV Now, the streaming product, which now has begun to outpace DirecTV subscriber growth, AT&T arguably was correct about DirecTV in key respects.

The fixed network upgrade to support U-verse was not going to happen fast enough to achieve critical mass. To get bigger, fast, AT&T was going to have to acquire that scale. And AT&T also needed an asset that would spin off free cash flow at significant levels, right away.

Growth by acquisition, in any case, has been the main driver of AT&T revenue growth for decades, so growth by acquisition obviously was a fit for AT&T company culture.

By acquiring DirecTV, AT&T instantly became the biggest linear video subscription provider in the U.S. market, something it was not going to be able to do by incrementally scaling up U-verse.

To be sure, there remain critics of AT&T’s effort to transform its business away from connectivity and towards apps and services beyond connectivity. The biggest clue is that AT&T now describes itself as a “modern media company.”

Financial analysts, in particular, are going to prefer a “stick to your knitting” approach that emphasizes connectivity products. Those of us who see that as a dead end will disagree. As difficult as it might be for AT&T and other tier-one service providers to transform themselves, reducing reliance on connectivity revenues, there is no other choice if survival as independent companies is the goal.

Not insignificantly, DirecTV boosted and supports AT&T cash flow, a strategic necessity for a firm that pays out high dividends, at scale, and whose value proposition for investors has been “steady dividend increases.”

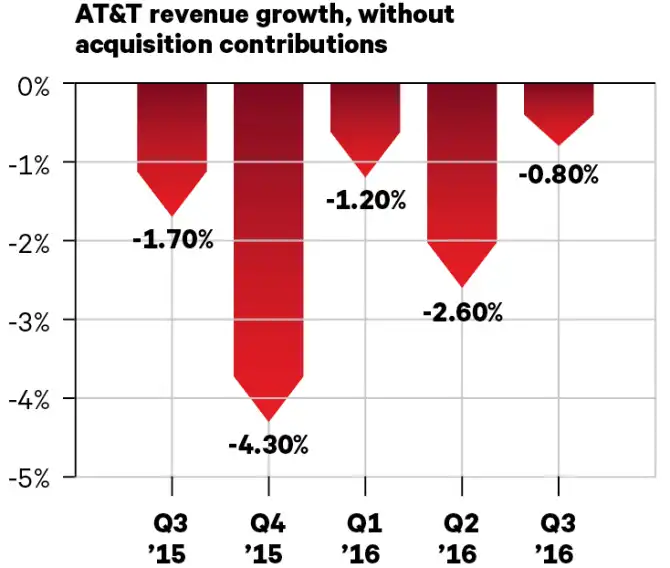

In fact, it is not incorrect to say that AT&T’s core businesses are relatively flat, in terms of revenue growth, and that most revenue growth has come from acquisitions.

Historically, over the last three decades, both AT&T and Verizon have grown revenue mostly by acquisitions. That arguably also is true for most tier-one service providers globally, and also for most small specialized carriers in the U.S. market. Organic revenue growth typically is not large enough, or fast enough, to support either continued high growth rates or the attainment of scale, which boosts profit margins.

The Time Warner acquisition boosted revenue about $31 billion, instantly. AT&T could not have gotten that big a boost organically, no matter what it had done. To be sure, debt loads now are an issue for both AT&T and Verizon, but that is likely to be an on-going issue, if one makes the assumption future growth will continue to be lead by acquisitions, and if at least some of those acquisitions must be large, to have any immediate impact on top and bottom lines.

No comments:

Post a Comment