Some numbers are underwhelming, even when touted as evidence of growth. If you were told that 370 enterprises globally were using local area networks, Wi-Fi, robots, internet-connected sensors, doing local computer processing or were connected to remote cloud computing facilities, would you really be impressed?

Would 370 enterprises globally using computing, software as a service, content delivery networks or some form of artificial intelligence or machine learning capabilities, strike you as terribly significant?

In other words, private 4G or private 5G networks are sort of like that. The use of typically “public network” technology to create a “private network” is important to public network infrastructure providers, as it creates an ancillary new market.

Private 4G or 5G networks might also drive some incremental revenue for public networking companies, who can design, build or operate such networks on behalf of enterprises.

Still, private network revenue is always dominated by infrastructure suppliers and systems integration suppliers. There seems little reason to think private 4G and 5G networks will deviate from that pattern.

Revenues from Wi-Fi as a service likely will still be in single-digit billions globally by about 2025, according to Markets and Markets.

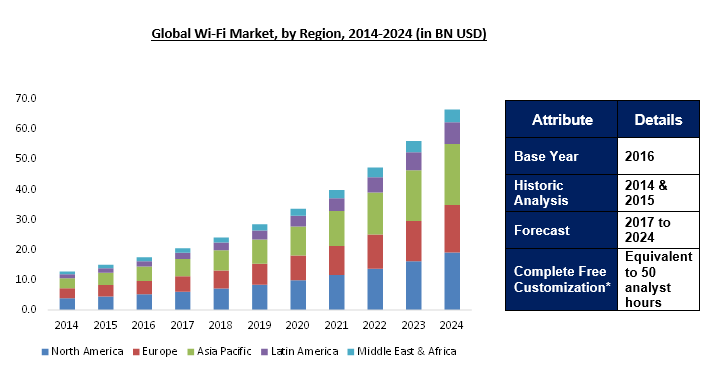

The Wi-Fi infrastructure market, on the other hand, might reach $66.5 billion in 2024, according to Ameri Research. In other words, managed services provided by all suppliers might represent 11 percent of total Wi-Fi sales activity in any given year.

No comments:

Post a Comment