“Owner’s economics,” the financial advantages for firms able to own--rather than rent--key inputs, often figures into service provider strategy. Quite often, ownership at scale is impossible for nearly all firms in the fixed networks business, though it has been possible for multiple mobile contestants to compete using owned facilities.

In most markets, it is thought unfeasible for multiple fixed networks to compete at scale, even if in some local markets that might be possible, to an extent, especially for specialized networks serving enterprise customers.

That has resulted in a reliance on wholesale policies to support retail competition, and in many markets, this has materially supported retail competition. What has proven much harder are incentives for investment on the part of the wholesale provider, not to mention other potential competitors.

Up to this point, both wholesale and facilities-based models have worked in the mobility segment of the business. The big question for policymakers has been the sustainability of facilities-based competition, and impact on consumer prices, between three or four contestants.

That was part of the review process for the T-Mobile US merger with Sprint, for example, leading to a compromise allowing the merger, on the condition that a fourth national contestant (Dish Network) also be created.

Dish Network has its own spectrum assets, but also will be able to rely on wholesale access to the T-Mobile US network for a period of time deemed long enough for Dish to build its own network.

Whether this happens, and what else might need to change to enable the creation of that network, is the issue. The approach is reminiscent of the “wholesale to encourage investment” strategy once undertaken by the U.S. Federal Communications Commission in deregulating the U.S. telecom market. That effort failed, which is the cautionary statement.

Telecom service provider wholesale policies can make or break business models. Back in the early years of the 21st century, U.S. regulators briefly relied on robust wholesale discounts--below actual cost, in many instances--for network service customers, in hopes of stimulating more competition in telecom services markets.

The policies allowed competitors to buy and use complete services--provisioned lines--to support competitive voice services. The framework allowed firms such as the then-independent AT&T and MCI to grow their retail phone services businesses.

It all collapsed when the Federal Communications Commission changed its rules and allowed network services suppliers to negotiate market-rate prices.

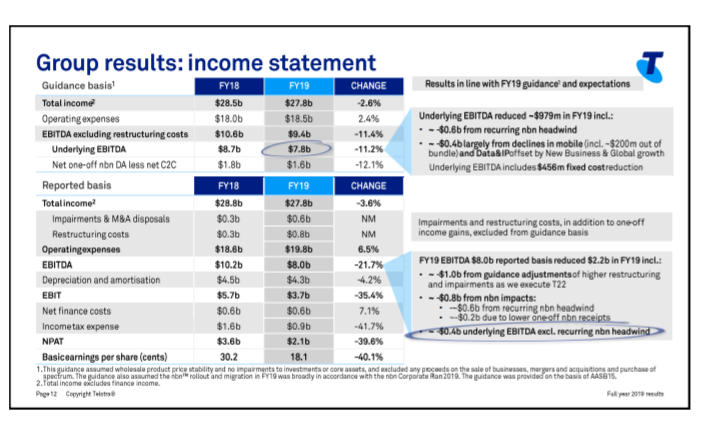

Australia seems to be suffering from a related problem with its National Broadband Network, as there is but one supplier of wholesale network services, leading Telstra to experience a 40-percent drop in profits, year over year.

The country’s largest service provider (which accounts for 41.5 percent of the telco industry’s market share) saw its profits plummet 40 per cent in the 2018-2019 financial year, largely because of NBN wholesale tariffs.

Telstra’s largest rival, Optus, similarly saw profits fall by 32 per cent in the same period.

That is one clear danger for all telecom regimes relying on a single wholesale network services supplier.The brief U.S. policy reliance on wholesale service supply--seen as a stepping stone to facilities investment--rather quickly was replaced by the alternative of facilities-based competition, and essentially worked because cable TV operators were able to use their own networks to compete in voice and internet access services.

The 1996 Telecom Act's focus had two goals: to open the local exchange market to competition (by stimulating facilities-based investment) and to promote expanded competition within the long-distance marketplace.

In retrospect, the focus on voice services--at a time when the internet was emerging--seems misplaced. A fundamental change in policy aiming to change voice market share was unveiled precisely at the point that voice services began a long-term decline.

The primary goal was to provide residential customers with choice and innovation in their local voice telephone service. After nearly seven years, though choice increased for urban customers, investment by the incumbent and competitive carriers was virtually nonexistent.

The problem is compounded by the decline of every legacy revenue stream the wholesale infrastructure is supposed to enable, with declining average revenue per user now a global trend.

Under such conditions, wholesale prices “need” to be reduced, as retail value is less, so retail price needs to decline. Whether that is possible, and to what extent, is the issue for the NBN.

Longer term, one has to ask whether that will be an issue for Dish Network as well. Dish will begin life with less than two percent market share, based almost exclusively on prepaid customers, the least desirable customer segment for any of the other three leading contestants.

What T-Mobile does fear--but many would argue must eventually happen--is the emergence of a deep-pocketed, strong brand name, new investor in Dish with a revenue model complementary to connectivity services.

Some believe that if Dish survives as a viable fourth competitor nationwide, it will because that new investor or owner emerges.

No comments:

Post a Comment