All else remaining equal, scale matters for any business in a competitive industry, but especially in any industry where network effects matter. And network effects matter for communications service providers and consumer app providers.

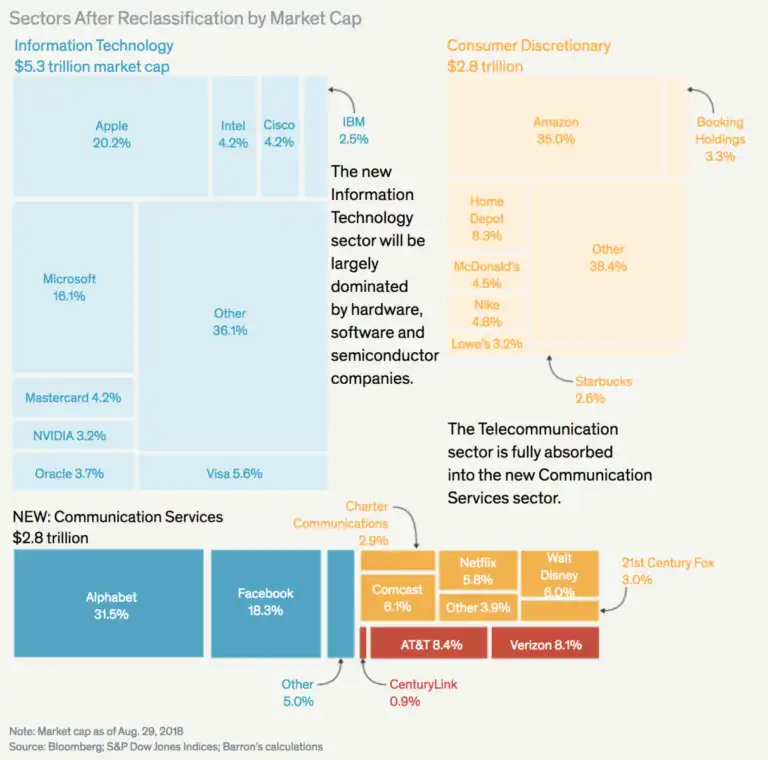

And one might note that even the largest U.S. connectivity services providers are small, compared to the biggest app and content suppliers. In the new Standard and Poors Global Industry Classification System (GICS), which will eliminate the “Telecommunication” sector of the system, and replace it with a new “Communication Services” sector, the biggest components--by equity value--will be Alphabet and Facebook.

The communication sector will include stocks from the information technology, consumer-discretionary, and telecom service provider areas. Alphabet, at 32 percent, will be the biggest entity in the index, followed by Facebook at 18 percent. Comcast, AT&T and Verizon will represent about eight percent each.

Disney and Netflix, at about six percent each, will also be in the index. But one might note that about half the value of the index is represented by Alphabet and Facebook.

And that, as much as anything, tells you how “communications” has changed, even if the move is prompted by other issues, such as the paucity of firms in the old Telecommunication index.

It simply is not possible anymore to cleanly delineate between a connectivity provider, an app provider or platform; between a content creator, a content owner or distributor.

Nor is it possible to miss the obvious: that the biggest app and platform providers are far larger than the largest connectivity providers. Also, several of the "connectivity" suppliers--notably Comcast and AT&T--already have made big moves into the content parts of the ecosystem.

Such numbers are among the reasons why many observers believe the old “connectivity revenues” business has to be augmented, in a powerful way, by involvement in new segments of the internet ecosystem. That is true for tier-one service providers in the retail business, but obviously might not be true for the many specialist roles within the connectivity business overall.

Such moves almost certainly will involve growth by acquisition, as organic growth alone will not suffice to replace perhaps half of all current revenue within a decade. In part, that is because legacy connectivity services revenues are flat or declining; in part because revenue per unit is declining; in part because those declines outpace the rate at which brand-new revenue sources can be created and grown, internally. Marginal cost pricing does not help, either.

Nor, in principle, can it be discounted that, eventually, connectivity providers will be potential acquisition targets themselves.

No comments:

Post a Comment