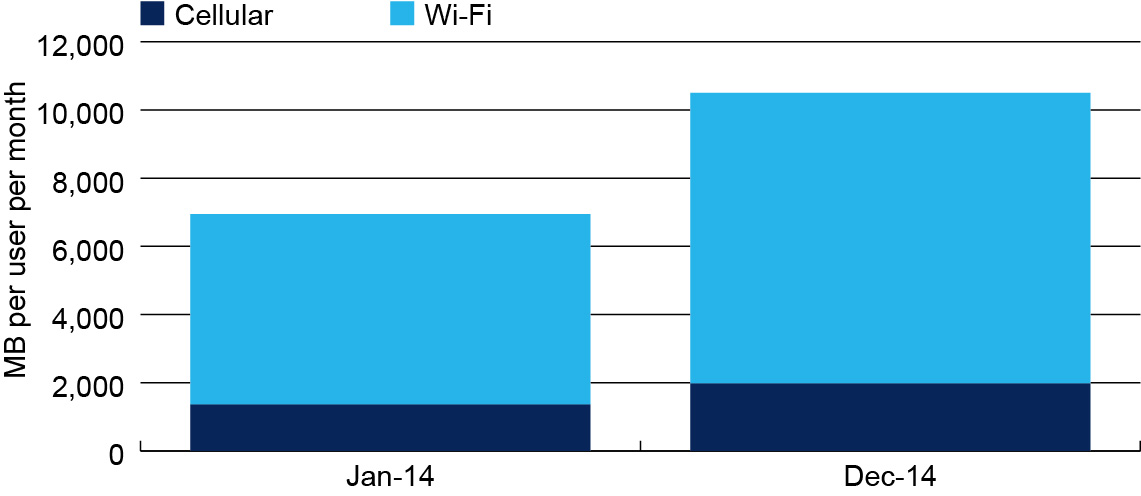

In some ways, it can be argued that Wi-Fi already is the “primary” access network for smartphone users, at least as measured by the consumption of data. About 80 percent of smartphone data is consumed on Wi-Fi connections, according to Mobidia.

That arguably is true even for voice communications and texting usage, about 80 percent of which also occurs when users are indoors.

To say that indoor usage is mostly defined by indoor locations does not necessarily capture “value,” however. Even if “usage” is not dominant when users are out and about, that setting might be the place where connectivity is most valuable.

That certainly historically was the great value of mobile phones. So what does it mean that most of the data, text messages or voice minutes of use happen indoors?

It is hard to say, at a time when the “primary” Wi-Fi connection virtually effortlessly switches to mobile network access whenever the user leaves an indoor location.

Cablevision Systems Corp. might be among the first service providers to find out how much value “mobility” provides, as its Freewheel service has no “mobile” backup. When out of range of Wi-Fi, the Freewheel phones simply will not work.

Craig Moffett, senior analyst at MoffettNathanson, argues that Wi-Fi will be the primary network in the future, while mobile networks are used only when users are out of range of Wi-Fi.

That is not hard to imagine. What might be harder to imagine is that a “mobile” service will get wide market share if no switch to mobile network access is possible.

It is one thing to say Wi-Fi handles most of the traffic volume. It might be another matter entirely to argue that customers will happily give up the ability to default to the mobile network.

Mobile Internet access traffic offloaded from mobile networks to Wi-Fi represented 45 percent of total mobile Internet traffic in 2013, and will grow to 52 percent of total mobile Internet access traffic by 2018, according to Cisco’s Visual Networking Index.

But some amount of share might be shifted, some think.

Jonathan Chaplin, a telecom analyst at New Street Research, does believe the more traditional “Wi-Fi first, switch to mobile” approach will work.

Wi-Fi-first mobile services offered by cable companies in the U.S. could shrink mobile service provider equity value by about 15 percent—or $68 billion—within five years after cable companies enter the mobile market.

But take note: that forecast assumes Wi-Fi first, but then a switch, automatically, to mobile access.

Nobody can yet guess what share could be possible for a Wi-Fi only service.